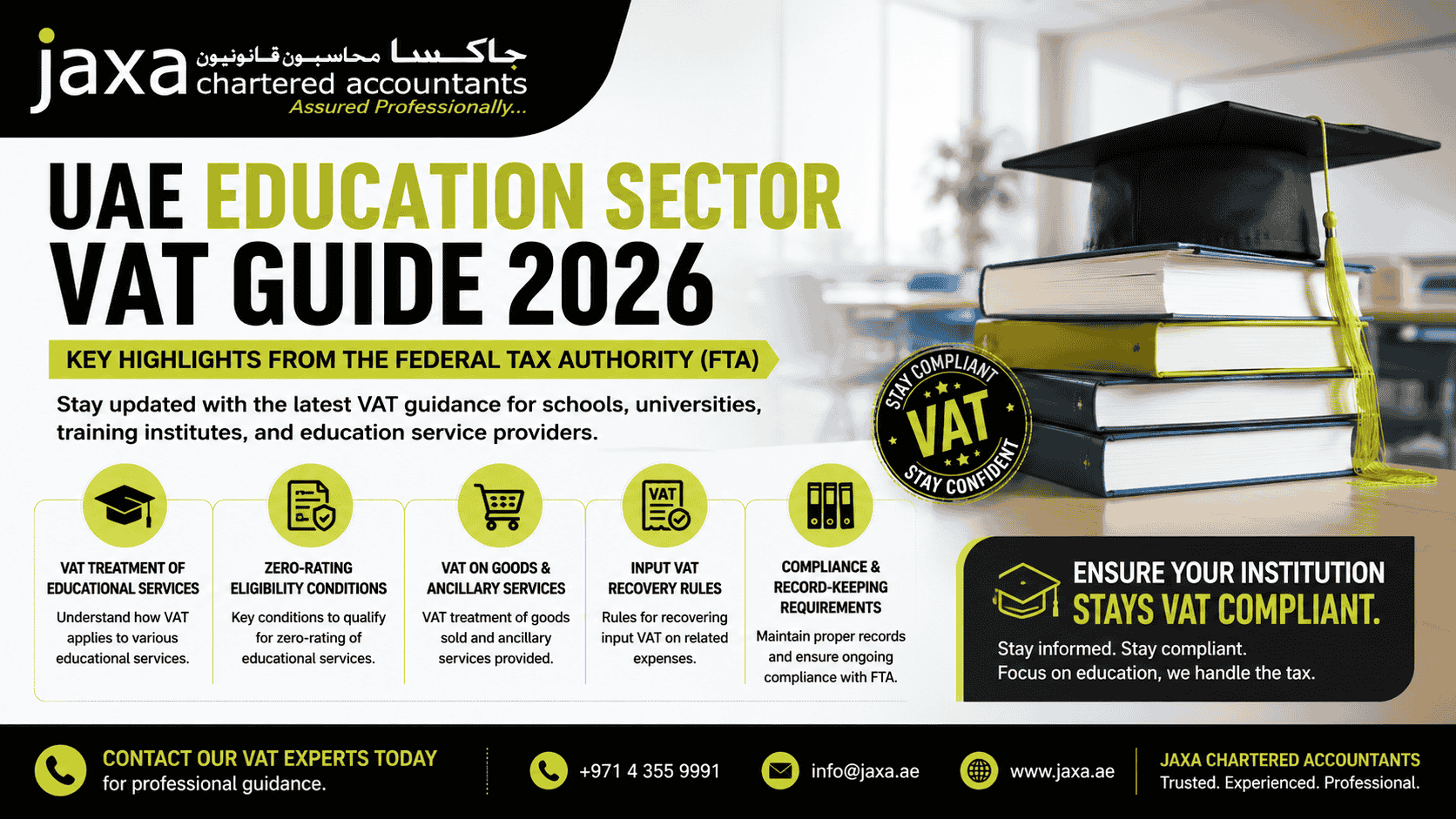

The UAE Federal Tax Authority (FTA) published the Education Sector Value Added Tax Guide (VATGED1) on June 29, 2026, providing detailed guidance on the VAT treatment of educational services, related supplies, and various activities carried out within the UAE education sector. Educational institutions, including schools, universities, nurseries, and training providers, should carefully assess the new guide to ensure compliance with UAE VAT rules.

The publication assists educational institutions in accurately understanding their VAT obligations, making informed tax decisions, and maintaining regulatory compliance. This guide explains which educational services qualify for zero-rate VAT, outlines the supplies that remain subject to the standard 5% VAT rate, and provides practical guidance on the VAT treatment of common transactions within the education sector.

Key Highlights of the UAE FTA’s Education Sector VAT Guide

The UAE FTA’s Education Sector Value Added Tax Guide (VATGED1) offers comprehensive clarification on the VAT treatment of educational services and related supplies. As educational institutions generate income from multiple sources, such as tuition fees, bus fees, event fees, annual fees, canteen fees, extra-curricular activities, each supply should be assessed separately to ensure accurate VAT treatment across all revenue streams as per UAE VAT legislation.

So educational institutions should review VAT treatment of all supplies, invoicing practices, and input VAT recovery to ensure compliance with the latest UAE FTA guidance.

Key reasons why this guide matters:

- Broad scope: This guide is intended for all persons and entities involved in supplying education services in the UAE

- Coverage of VAT classification: Explains the VAT treatment of tuition fees, student accommodation, transportation, digital learning, grants, scholarships, research activities, and other education-based transactions.

- Applying correct VAT treatment: This guide helps institutions determine which supplies qualify 0% VAT rate, when the standard 5% the VAT rate applies, and how input VAT should be recovered.

- How the guide should be used: The UAE FTA states that the guide serves as an administrative guidance and should be read together with the UAE VAT law and VAT executive Regulations.

Key Highlights of the FTA’s Education Sector VAT Guide

- Zero-rated educational services:

Being an educational institution does not automatically mean your services are zero-rate VAT. To apply the 0% VAT rate, an educational institution must first meet the criteria of a qualifying educational institution under UAE VAT regulations.

Qualifying educational institutions include:

- Nurseries and preschools

- Primary and secondary schools.

- Colleges, universities, and higher education institutions.

To be treated as a qualifying educational institution, an institution must meet the eligibility requirements per UAE VAT rules.

- An educational institution is recognised by the federal or local competent Government Entity regulating the education sector in the relevant Emirate in the UAE.

- Higher education institutions are only eligible if they are owned by the federal or local government, or receive more than 50% of their annual funding directly from the federal or local government. Where a higher educational institution receives funding from more than one federal or local government source, the aggregate amount received should be more than 50% in order to meet this condition.

- Educational Services must be provided in accordance with a curriculum recognised by the federal or local competent Government Entity regulating the education sector in the relevant Emirate in the UAE.

If these eligibility criteria are met, qualifying educational services, including tuition fees and certain curriculum-related material, can be supplied at the 0% VAT rate.

Proper documentation is required to support zero-rated VAT treatment. Educational institutions should retain evidence of their official recognition and government ownership or funding.

Qualifying Curriculum

The VAT treatment of educational services in the UAE depends on whether they are delivered under a recognized curriculum approved by the relevant education authority. While qualifying educational programmes may benefit from 0% VAT rate, services such as executive education, short-term diplomas, skill development courses, and private tuitions are subject to the standard 5% VAT rate.

- VAT on Related Goods and Services

The UAE’s FTA guide clarifies that VAT treatment of goods and services supplied by educational institutions depends on the nature of the supply. While some items directly connected to qualifying educational services may be eligible for the 0% VAT rate, others are either exempt or subject to the standard 5% VAT rate.

Key compliance consideration:

When evaluating the VAT treatment of education-related charges, institutions should consider:

- Whether the supply is directly linked to a qualifying educational service

- Whether it forms part of a recognized curriculum in the UAE

- Whether the student is enrolled in the qualifying educational institution.

Examples of related supplies include:

- Printed and digital learning materials

- School accommodation

- School transportation

- Meals for students

- School uniforms

- Examination fees

- Administration and registration fees.

Key examples:

- Curriculum-related supplies: Printed and digital learning materials, a curriculum-based field trip may qualify for zero-rated VAT.

- Non-qualifying supplies: School uniform, electronic devices, food and beverages, and optional extracurricular activities are subject to the standard 5% VAT rate.

- Purpose of the supply: A field trip that forms an integral part of the approved curriculum may qualify for zero-rating, whereas a recreational excursion organized by the same institutions is taxable at standard 5% VAT.

| Education-related charge | VAT treatment under the 2026 FTA guide |

| Application fee | Standard rate 5% VAT, where the applicant is not yet enrolled |

| Re-registration fee | May qualify for 0% VAT rate if directly connected to qualifying educational services |

| Graduation fee | May be zero-rated if linked to a qualifying education |

| Education-linked field trip | May be zero-rated if they are curriculum-related and not primarily recreational |

| Uniforms, devices, meals, and optional activities | Generally subject to the standard 5% VAT rate |

The UAE FTA highlights the necessity of keeping consistency in VAT reporting. Educational institutions should ensure all fee schedules, invoices, credit notes, and financial records accurately reflect the VAT treatment applied to each transaction.

As these supplies are subject to their own VAT rules, educational institutions should evaluate each type of supply separately to determine whether it qualifies for the 0% VAT rate or is subject to the standard 5% VAT rate in accordance with UAE VAT legislation and FTA’s guidance.

- Digital Learning, Grants, and Research Funding

The UAE VAT education Sector Guide provides key clarification on the VAT treatment of digital learning, grants, donations, and research funding. As the VAT treatment depends on the specific facts of each arrangement, educational institutions should evaluate every transaction carefully.

- Digital learning: Online courses delivered with minimal human interactions, such as pre-recorded lectures or automated assessments, may be treated as electronic services for UAE VAT purposes.

- Live online teaching: Live classes such as online lectures, tutor interaction, and personalized feedback are treated as educational services. If all qualifying conditions are met, it may qualify for 0% VAT rate.

- Grants and donations: A grant or donation may be subject to UAE VAT if the payer receives a direct or identifiable benefit in return.

- Research funding: If the funder receives intellectual property rights, commercial exploitation rights, or other direct benefits, the payment may be subject to the standard 5% VAT rate.

The latest UAE FTA guidance reinforces the need for educational institutions to assess digital learning services, grant funding, and research agreements individually to ensure accurate VAT classification and compliance with UAE VAT rules.

- Input VAT recovery for the UAE education sector

The UAE FTA Education Sector VAT Guide delivers significant clarification on input VAT recovery for educational institutions in the UAE. As many schools, universities, and training providers make a combination of taxable, zero-rated, exempt, and non-business supplies, it is important to determine how to recover input VAT.

Key rules for input VAT recovery:

- Recoverable input VAT: Input VAT is recoverable where goods and services are used or intended to be used to make taxable supplies, including zero-rated supplies.

- Exempt and non-exempt activities: Input VAT attributable to exempt supplies or non-business activities is generally not recoverable.

- Mixed-use expenses: Where costs relate to both recoverable and non-recoverable activities, institutions may need to apply an input VAT apportionment method in adherence to the UAE VAT regulations.

- Restricted input: This guide highlights that VAT incurred on certain expenses, such as business entertainment or school buses used for exempt local passenger transport, may not be recoverable.

So, educational institutions should properly review their input VAT recovery methodology to ensure it accurately reflects the use of their expenses and complies with the latest UAE FTA education Sector VAT Guide.

Steps to be taken by Educational Institutions pursuant to this new FTA Guide

Following the release of the UAE FTA education Sector VAT guide, educational institutions should take proactive steps to ensure compliance with the latest UAE VAT requirements. This includes:

- Review the VAT treatment of all educational services and related supplies

- Confirm eligibility for the 0% VAT rate on qualifying educational services

- Verify the VAT treatment of ancillary supplies, including transportation, accommodation, meals, and learning materials

- Assess input VAT recovery and apportionment methods

- Maintain proper documentation to support the AT treatment applied

- Update VAT policies, invoicing procedures, and accounting records where necessary.

Conduct a VAT health check to identify potential compliance gaps, reduce VAT risks, and ensure compliance with the latest UAE FTA guidance.

Why is compliance necessary?

Applying the incorrect VAT treatment may result in:

- Additional VAT assessments

- Administrative penalties

- Interest on unpaid VAT increased scrutiny during FTA audits

While reviewing the new guidance and aligning internal processes properly, educational institutions can strengthen compliance with confidence.

How Jaxa Auditors, the best VAT consultant in the UAE, can help

Navigating the latest UAE VAT regulations for the education sector requires a thorough understanding of the UAE FTA Education Sector VAT Guide and UAE VAT legislation. Reviewing your VAT position with professional guidance can help prevent costly penalties.

Jaxa Chartered Accountants, an FTA-approved tax agent in the UAE, as well as accounting and auditing firms across the UAE and Dubai, help educational institutions understand and apply the latest UAE VAT requirements.

Our VAT experts in Dubai assist clients with:

- Reviewing the VAT treatment of educational services and related supplies.

- Assessing eligibility for zero-rate VAT

- Evaluating input VAT recovery and apportionment methods

- Conducting pre-VAT health check and compliance reviews

- Preparing and filing UAE VAT returns

- Representing clients before the FTA during audits, reviews, and tax assessments

With over 19 years of experience, Jaxa Auditors delivers practical and valuable VAT solutions that help educational institutions remain compliant with the latest UAE FTA guidance while reducing VAT compliance risks.

Need help while applying the new UAE FTA VAT guide?

Don’t let complex VAT rules impact your institution. Get in touch with Jaxa Auditors for expert VAT advisory and help you implement the latest FTA guidance.

Check out our VAT services page for more updates.