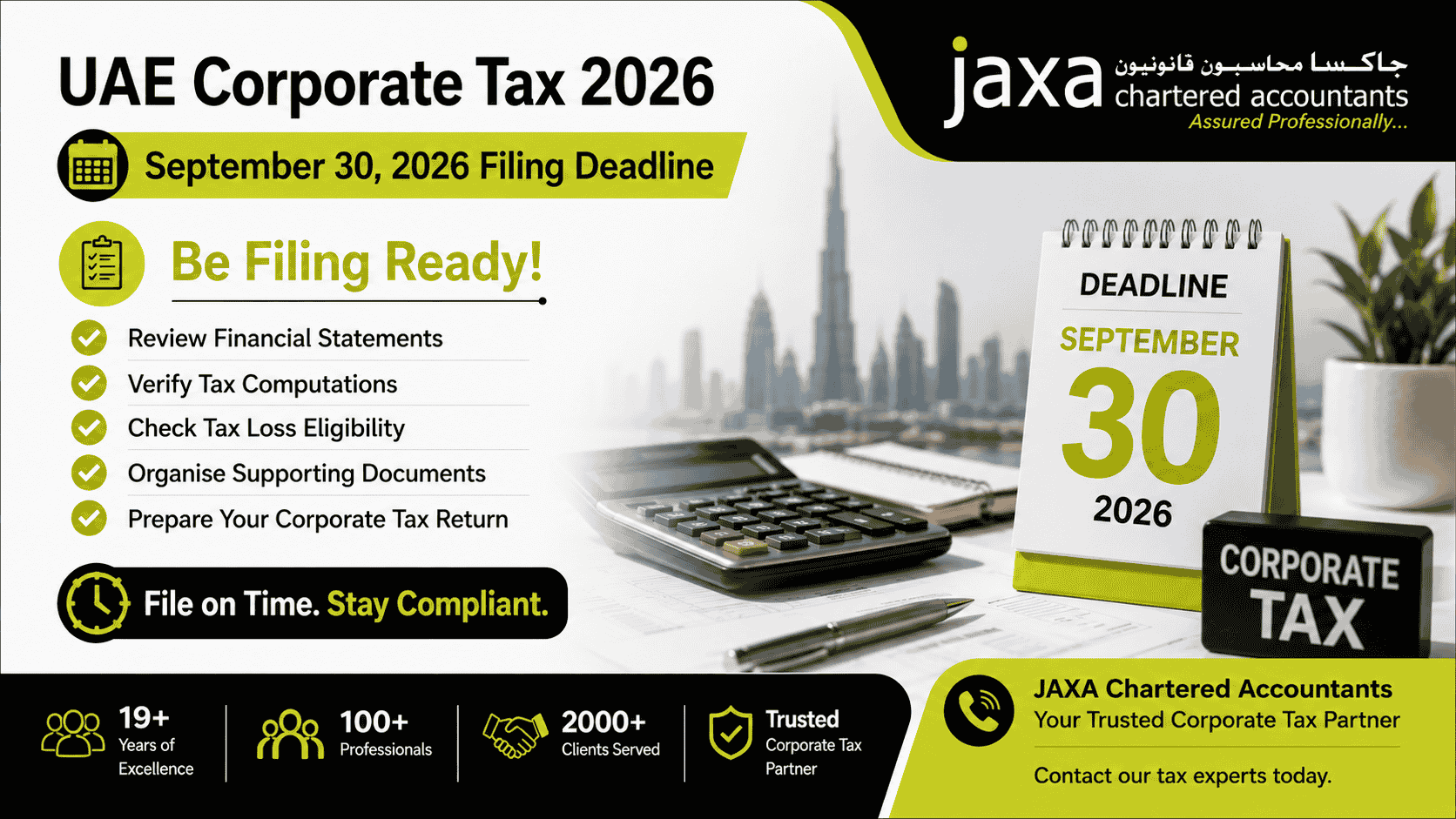

The UAE corporate filing deadline 2026 is an important compliance milestone for businesses across the Emirates. Whether you are preparing for your first tax return or managing ongoing compliance, having a well-structured UAE corporate tax filing checklist can help mainland and free zone companies ensure accurate reporting, timely submission, and complete compliance with UAE FTA requirements. Meeting corporate tax obligations on time is essential to avoid penalties and maintain compliance.

For businesses with a financial year ending on 31st December 2025, the UAE corporate tax return and payment must be submitted by 30 September 2026 to ensure timely compliance, review their financial records, prepare the necessary documentation, and complete filing requirements before the deadline.

In this article, we’ll walk you through everything you need to know about the UAE corporate tax filing deadline 2026, including key documents, important deadlines, common mistakes to avoid, and practical tips for staying compliant. If you need assistance from the best corporate tax assistance in the UAE, Jaxa Chartered Accountants provides end-to-end corporate tax services, helping ensure accurate filings, regulatory compliance, and peace of mind.

What is UAE corporate tax, and Who Needs to file?

Under Federal Decree No.47 of 22, the UAE Corporate tax is a key compliance obligation for businesses operating in the UAE. As per the UAE corporate tax framework, most taxable persons must register with the UAE FTA and file an annual tax return. Eligible entities are required to maintain proper financial records and submit an annual corporate tax return.

The UAE corporate tax system requires businesses to accurately determine their tax liability, file returns on time, and settle any outstanding tax obligations on time.

If a business is subject to the 0% Corporate Tax rate on taxable income up to AED 375,000, it is generally still required to file a UAE corporate tax return and comply with the FTA’s filing requirements.

The filing requirements generally apply to:

- UAE mainland companies

- Free Zone entities

- Foreign companies with a taxable presence, such as Branches and permanent establishments in the UAE

- Eligible individuals carrying out business activities

When Is Your UAE Corporate Tax Return Due? Key Filing Deadlines

Most taxable persons under UAE Corporate tax are required to file one corporate tax return per tax period, usually aligned with their financial year, with the filing deadline falling nine months from the end of the relevant tax period as prescribed by the UAE FTA.

The corporate tax filing deadline in the UAE varies based on your financial year-end.

For instance,

Businesses with a financial year ending 31st December 2025 must file by 30 September 2026.

Those businesses with a financial year ending 31 March 2026 must file by 31st December 2026.

In addition to submitting the tax return, any corporate tax liability must be paid by the same filing deadline.

UAE Corporate Tax Return Pre-Filing Checklist

Before filing a UAE corporate tax return, businesses should complete all necessary preparation steps to ensure accurate reporting and compliance with UAE FTA requirements while reducing the risk of errors and penalties.

The pre-filing checklist is as follows:

- Confirm whether your business must file a UAE corporate tax return:

- All taxable persons in the UAE are required to file a corporate tax return, including resident companies and non-resident entities with permanent establishment.

- Filing is mandatory unless the business is specially exempt under the UAE corporate tax. .

- Businesses with annual revenue up to AED 3 million may qualify for Small Business Relief (SBR), which can simplify compliance and documentation requirements. Eligibility for SBR requires a simplified corporate tax return filing.

- Review whether your business has a free zone status and qualifies for 0% tax on qualifying income.

- Ensure proper classification of business activity to determine taxable vs exempt income.

- Refer to FTA guidance on taxable persons and filing requirements for accurate determination.

- Prepare financial statement:

Preparation of accurate financial statements is essential for UAE corporate tax compliance. Companies must maintain IFRS-based financial records, including balance sheets and profit and loss statements, to support corporate tax returns.

- Compute taxable income: Under the UAE corporate tax regime, taxable income is derived by adjusting accounting profits based on prescribed tax rules and allowable deductions.

Some key adjustments:

- Adding back non-deductible expenses such as penalties, fines, and entertainment-related costs.

- Deducting exempt income, including qualifying dividends

- Applying 0% tax on income up to AED 375000 and 9% on income above the threshold.

Keeping proper documentation and working papers throughout the financial year is essential to ensure accurate tax computation and compliance.

- Review applicable relief and exemption: Businesses should assess eligibility for available corporate tax relief, such as:

- Small business relief for eligible entities with revenue thresholds

- Free zone person relief for a qualifying person subject to conditions under the UAE corporate tax law.

- Transfer pricing exemption, where applicable under the UAE corporate tax law

All relief must be carefully assessed and properly supported with documentation, as taxpayers are required to make a formal declaration while filing a corporate tax return.

- Gather key documents

All relevant financial and tax records should be organized in advance, including:

- Tax Registration Number (TRN)

- Financial statement and trial balance

- General ledger and accounting records

- Fixed asset register with depreciation schedules

- Contracts, invoices, and loan agreements

- Transfer pricing documentation

Well-organized documentation helps streamline the filing process an serve as supporting evidence in the event of future FTA review or audit.

- Final review before filing: Before submitting a UAE corporate tax return, the business should verify whether the financial data is correctly calculated and accurate to ensure compliance with UAE corporate tax regulations

Key review include:

- All financial information is complete, accurate, and properly reconciled

- Taxable income has been correctly computed as per the UAE corporate tax

- All applicable reliefs and exemptions have been correctly identified and applied

- Supporting documentation is complete, organized, and easily accessible.

This step is essential to reduce errors, avoid penalties, and ensure smooth compliance with UAE corporate tax regulations.

Step-by-step corporate tax filing checklist UAE – 2026

- Registering corporate tax: Ensure your business is registered for UAE Corporate Tax through FTA’s Emaratax portal. Registering for Corporate tax is mandatory, and failure to register on time may result in administrative penalties.

- Organize financial records: Before filing, ensure that all accounting records have been reconciled and that financial statements are accurate and comply with IFRS accounting standards.

- Supporting evidence: Maintain invoices, contracts, and documents supporting income and expenses.

- Calculate taxable income after adjusting accounting profit for disallowed items, exemptions, and reliefs to determine taxable income.

- Complete and verify corporate tax return: accurately complete and review the corporate tax return on the Emaratax portal.

- Submit return and settle tax liability: Submit corporate tax filing before the applicable deadline and pay any corporate tax liability.

- Maintain records: All financial records, tax computations, and supporting documents must be retained for at least seven years to comply with the UAE tax record-keeping requirement.

Some common UAE Corporate tax filing Mistakes to Avoid

Even a well-managed business can face challenges when preparing corporate tax returns. Identifying and avoiding common errors can help reduce compliance risk and minimize the chance of penalties.

Some of the most common filling errors include:

- Delaying corporate tax preparation until the end of the filing deadline

- Preparing inaccurate tax calculations

- Misclassifying exempt or qualifying income

- Incorrect assessment of the qualifying free zone person eligibility

- Neglecting transfer-pricing documentation obligations

- Failure to avail applicable reliefs in the CT return

Conducting a thorough review before submission can help identify potential issues and ensure compliance with UAE corporate tax requirements. For businesses seeking expert guidance, Jaxa Auditors can assist with tax computation, compliance reviews, return preparation, and filing support to help minimize risks and ensure accurate reporting.

What happens if you miss a UAE corporate tax deadline?

Businesses that fail to meet UAE corporate tax obligations may be subject to administrative penalties. Some penalties are as follows:

- Last filing penalty: AED 500 per month (or part thereof) for the first 12 months of delay.

- Increased late filing penalty: AED 1000 per month (or part thereof) from the 13th month onwards.

- Late corporate tax payment consequences: Additional charges may apply to unpaid corporate tax liabilities as per FTA regulations.

- Incorrect tax return submission: penalties may be imposed for errors, omissions or inaccurate information in a corporate tax return.

- Failure to maintain the required records may lead to non-compliance penalties.

- Not providing information requested by the UAE FTA may result in fines

- Repeated non-compliance may increase the likelihood of future tax audits.

Practical tips for smooth UAE corporate tax filing

- Start preparing for your corporate tax return well before the filing deadline.

- Maintain accurate financial records and supporting documents throughout the year.

- Ensure taxable income calculations are reviewed for accuracy

- Engage with a professional tax advisor in the UAE for complicated corporate tax matters.

- Retain financial and tax records for at least seven years

- Monitor corporate tax deadlines and keep your Emaratax profile updated.

Careful preparation and review are essential for successful corporate tax compliance. Jaxa Auditors offers expert corporate tax services in Dubai to help businesses navigate FTA requirements and ensure accurate, timely filing.

Prepare early and file your UAE corporate tax return with confidence

Meeting the September 30, 2026, corporate tax filing deadline is essential for maintaining good standing with the UAE Federal Tax Authority. While this checklist serves as a guide, businesses should assess their financial and tax position to ensure complete accuracy. Establishing a well-organized compliance process throughout the year can improve accuracy and reduce last-minute pressure.

For reliable corporate tax and VAT compliance in the UAE, partnering with an experienced UAE FTA tax agent is highly recommended. With 19 years of expertise in accounting, auditing, and taxation in the UAE, Jaxa Auditors helps clients to ensure compliance and accuracy across all financial obligations.

We assist clients with:

- Corporate tax compliance in the UAE

- VAT compliance in the UAE

- Emaratax filing and submission

- Corporate tax and VAT registration in the UAE

- Transfer pricing advisory assistance

- Free zone advisory support

Avoid penalties and file with confidence. If you need any assistance for corporate tax filing and compliance in the UAE, best firms like Jaxa Chartered Accountants is always there to assist you.

Book for a Free Consultation

FAQ

- Is it mandatory to file UAE Corporate tax if there is no profit?

Yes, all registered taxable persons in the UAE are required to file a corporate tax return, even if taxable income or profit is zero.

- Are free zone companies exempt from the corporate tax filing requirement?

No, all qualifying free zone persons must file a return, even if they enjoy 0% Corporate tax.

- What is the record retention period for UAE corporate tax?

Taxpayers must keep all relevant records for at least seven years after the tax period ends.

- Do all companies in a group file on the corporate tax return in the UAE?

They can only file jointly if they form an approved tax group, individual returns are mandatory.