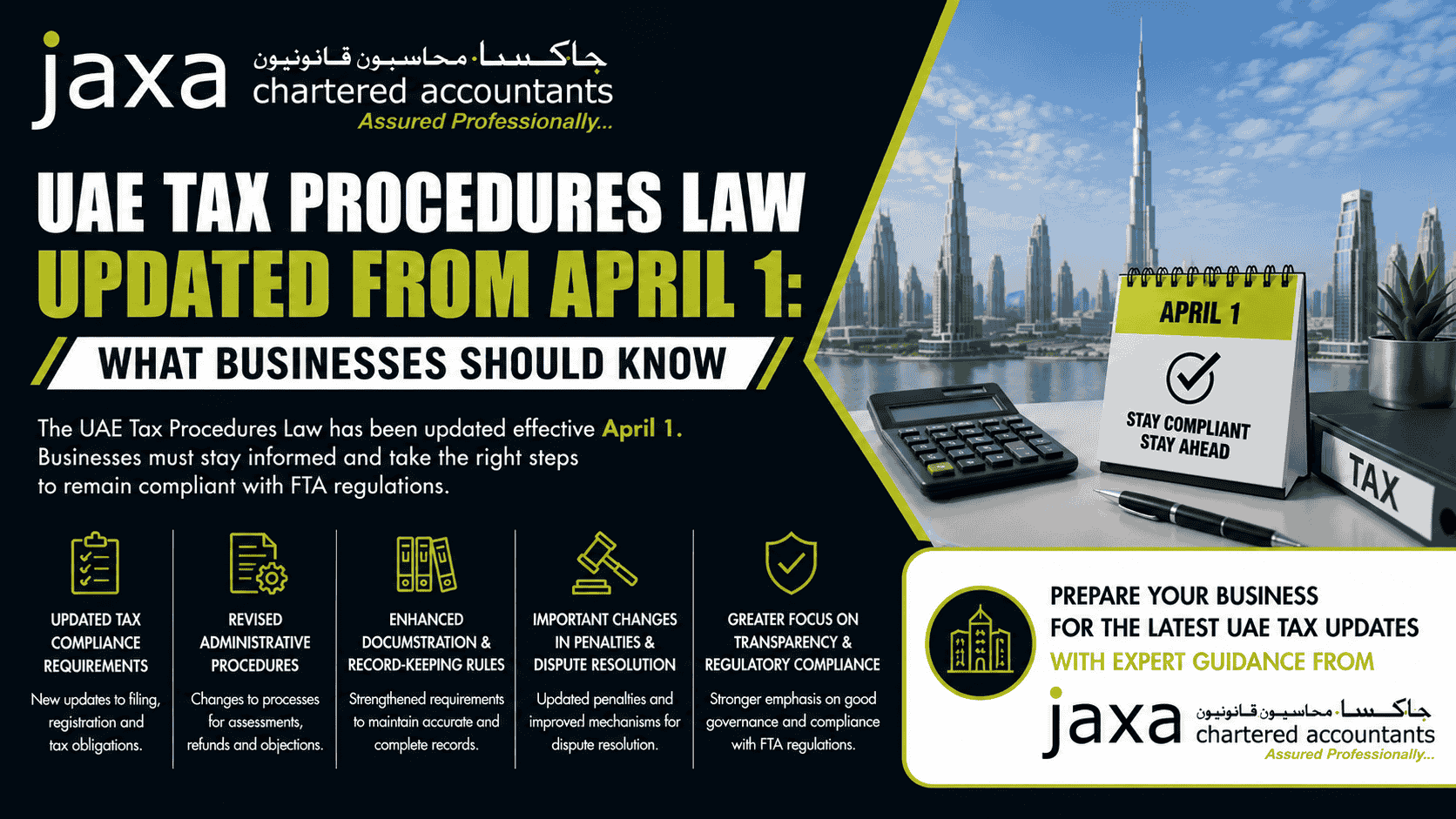

The UAE Ministry of Finance and the Federal Tax Authority have issued important regulatory updates through Cabinet Decision No. 17 of 2026, effective from April 1, 2026, amending key provisions of the Executive Regulation of the UAE Tax Procedure Law, which governs tax procedures and compliance obligations for businesses. Building on the amendment effective from 1st January 2026, these updates aim to streamline tax procedures, strengthen transparency, and ensure consistent tax enforcement across the UAE.

These updates are applicable across UAE VAT and corporate tax, addressing improvements to refund procedures, voluntary disclosure, record-keeping obligations, audit readiness, and enhanced taxpayer data confidentiality. Staying informed about these updates is crucial for businesses and taxable persons to remain compliant and prevent administrative penalties.

Understanding the technical nature of these amendments requires assistance from professional tax advisors, such as Jaxa Chartered Accountants, a UAE FTA tax agent, to ensure accurate implementation and compliance. In this blog, we highlight the major tax procedure updates effective from April 1, 2026.

Overview of UAE Tax Procedure Amendments Under Cabinet Decision No. 17 of 2026

The UAE Ministry of Finance has introduced amendments through Cabinet Decision No. 17 of 2026, updating key provisions of the Tax Procedures Executive Regulation. The key changes are outlined below:

-

New Record-Keeping Rules for Refund Claims

One of the notable updates regarding the documentation retention period is maintaining the five-year retention rule while introducing a new provision for ongoing refund applications.

New provision: A taxable person must retain books and records for an additional two years if a refund application is under review by the UAE FTA, provided the refund claim was submitted within five years from the end of the relevant tax period.

Jaxa Insights: The updates reinforce the need to keep all supporting refund-related records readily available for audit review until the UAE FTA finalizes its refund assessment.

-

Revised Voluntary Disclosure guidelines:

The Executive Regulation issues clear guidance on the treatment of erroneous refund claims. This updated provision has refined the responsibility of the taxable person while identifying discrepancies in the tax returns or assessments.

Error Reporting Thresholds

- If the error exceeds AED 10,000, then the Voluntary Disclosure must be submitted within 20 business days of identifying the discrepancy.

- If the error is AED 10,000 or less, it might be adjusted in the next eligible tax return or through voluntary disclosure, where no return is available.

- In case no subsequent tax return is required to be filed, the taxpayers must still submit a voluntary disclosure within 20 business days from the date of identifying the error.

Jaxa compliance Note: The revised rules emphasize the need for effective refund control processes, ensuring that taxpayers are advised to promptly detect and correct errors within the regulatory timeline, especially where the AED 10,000 threshold requires mandatory voluntary disclosure.

-

Credit Balance Refund Procedure

The updated regulation replaces the term “ tax refund” with “refund of credit balance” to align with the UAE Tax Procedure law. Article 26 defines the timelines for handling refund applications.

- Statutory timeline for refund decision: The UAE FTA is required to review the refund application and notify the taxpayers of the outcome within 20 business days.

- Refund repayment timeframe: Once the UAE FTA approves the refund, the authority is obligated to process and initiate the repayment within 5 business days from the date of notification.

- Deferred tax return: The UAE FTA may deter or withhold refund payments if the taxpayer has outstanding tax returns that remain unsubmitted.

Jaxa Advisory Note: The term “ refund of credit balance” clarifies that all excess tax amounts are eligible for the scope of refund procedures. To avoid delays, taxpayers are advised to maintain well-documented credit records and timely filing of returns, as outstanding filing or missing records may affect the smooth refund processing.

-

Updated Provisions on Seizure of Documents and Assets

The revised amendments empower FTA to extend the duration for holding seized documents or assets, subject to notifying the concerned party whenever applicable. This enables the authority’s ability to completely review the process.

Jaxa Insights: Businesses are advised to strengthen audit preparedness, ensure document accessibility, and implement backup plans to prepare for possible business disruption arising from a prolonged retention period.

-

Confidential data sharing provision:

The 2026 amendments introduce revised provisions regarding the disclosure of taxpayer information to government authorities, which require formal agreements ensuring proper confidentiality and data protection.

Jaxa Insights: This provision emphasises the need for handling and protecting sensitive business and financial data to reduce regulatory and reputational risk.

What the New Tax Rules Mean for Business Compliance in the UAE

The latest tax amendments bring several compliance implications for businesses operating in the UAE. To maintain regulatory compliance and mitigate penalty risk, businesses should review and enhance the tax process, document management practices, and internal control systems.

Key focus areas are:

- Timely error identification: Regular internal checks should be carried out to spot and fix errors in UAE VAT and corporate tax filings to ensure a timely compliance process.

- New record retention rules: Organizations must retain financial and tax records for extended timelines for VAT refunds, audit, or tax assessment.

- Audit-ready digital storage: The business must keep digital backups of key financial and tax records to ensure smooth access during audits and reviews.

- Team awareness of tax updates: Regular updates and training should be given to the tax, accounting, and finance teams on new amendments to ensure proper implementation and proper compliance.

- Support from tax advisors: Engaging with UAE tax consultants & advisors, such as Jaxa Auditors, a UAE FTA tax agent with 19+ years of experience, allows businesses to respond effectively to regulatory changes and strengthen their compliance framework while mitigating compliance risks.

Key takeaway

The 2026 amendment enhances the UAE tax framework through stricter compliance timeliness, extended audit power, enhanced compliance discipline, and proactive tax management, requiring businesses to remain vigilant and well-prepared in managing tax obligations.

Jaxa Chartered Accountants, a UAE FTA tax agent and a leading accounting and taxation firm, ensures that every compliance requirement is accurately reflected in your financial records. Our tax agents in the UAE seamlessly track regulatory developments in the UAE to provide clients with up-to-date compliance support. We ensure that these updates are implemented directly into your compliance and accounting system, allowing you to operate with confidence and peace of mind.